Why Southeast Europe Is Our First European Market: Bulgaria, BESS and Entering from the Edge

Europe set a record 27.1 GWh of new batteries in 2025 — but the real story is the gravity moving to utility-scale and C&I. Bulgaria became the EU's #3 market (+1,200%). Why N2N enters Europe from Southeast Europe, as an asset-light software layer.

When people read Europe's energy-storage numbers, most fixate on a single figure: 27.1 GWh of new batteries installed in 2025. It's an impressive number — a 12th straight record year, up 45% year-on-year (SolarPower Europe). But looking at that table, what caught our attention was not the total. It was the shift underneath it. And honestly, that shift decided where and how we enter Europe.

Europe set a record — but the real story is the gravity moving

27.1 GWh sounds big, and the cumulative fleet now stands at 77.3 GWh. But the picture changes when you go down to segments. In 2025, 55% of new capacity was utility-scale — the first year it outpaced residential. The commercial and industrial (C&I) segment grew 31% to 2.3 GWh. Residential storage, by contrast, fell 6% to 9.8 GWh — its second straight annual contraction.

This is not an abstract statistic for us. Orchestration software follows the asset. If the money moved from residential home batteries to utility-scale and C&I assets — and the data says exactly that — an EMS/DERMS provider should put its priority there too. So that is what we did: residential is a side product for us; our main engine is C&I (Pulsar) and utility (Quasar).

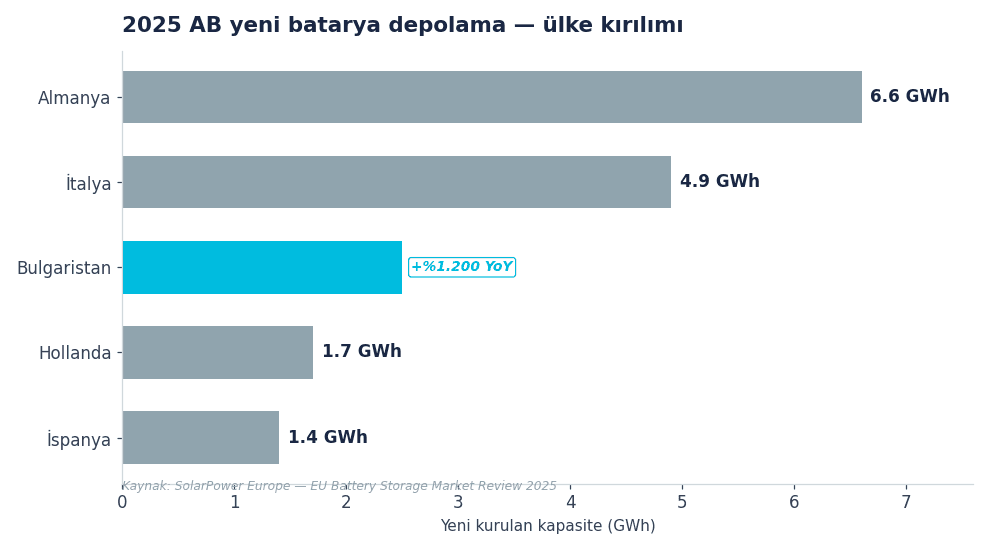

Bulgaria: the third-largest market nobody talks about enough

Here is the interesting part. Ask who Europe's three biggest storage markets were in 2025 and most people, after Germany and Italy, say Spain or the UK. The answer is Bulgaria. With 2.5 GWh of new capacity it became the EU's third-largest market — growing roughly 1,200% year-on-year (SolarPower Europe).

A single annual jump could be dismissed. But the whole region around Bulgaria is moving the same way. Central and Southeast Europe is forecast to take more than half of the EU's smart-meter shipments by 2029 (up from 28% in 2023). Nine of the ten fastest-growing first-generation markets are in this region. Bulgaria is not a one-off spike; it is the leading edge of a broader wave.

Why Southeast Europe first — by openness, not by size

Most companies make the market-entry call by size: the biggest market is right there, so start there. We look at a different criterion — how open the field is.

Because the biggest markets tend to be the most crowded and the most mature: incumbents, saturated competition. There is also the infrastructure side: in some large markets, household smart-meter penetration is still very low (Germany, for example, at around 1% — smartEn), and independent-aggregator wholesale access is currently fully open only in France and Great Britain. In other words, "biggest" doesn't always mean "most ready."

So we act on that criterion: we start where growth is fast, competition is low, and the door is open — and Southeast Europe is a clear example of that for us. Win a real reference where the field is open, then grow on the back of that proof. Better early in an open market than late in a crowded one.

Asset-light: we don't finance the steel, we make it earn

Let's answer the question we get most: "So who finances the battery?" Not us. And that is the point.

We are asset-light on purpose. We do not own the steel — the battery, the inverter, the container — or carry it on our balance sheet. We are the software layer that makes someone else's solar+storage asset earn its return; hardware-neutral, working with any inverter and any BESS. There is a reason: asset-heavy energy is a capital trap, especially for a small software team. The asset itself keeps getting cheaper; the intelligence that makes it earn does not. We would rather be the intelligence on top of the asset than the debt underneath it.

What we actually solve on site

For an IPP or a C&I owner in Southeast Europe, this means, concretely:

On the utility side, Quasar runs GES+BESS plants from a single control layer — grid-scale dispatch, ancillary services and portfolio optimization. On the C&I side, Pulsar runs behind-the-meter solar+storage autonomously — hourly-market arbitrage, peak shaving, demand-charge control and compliance reporting. Both hardware-neutral, both built to make an asset earn — not to sell you another box.

Our first European site fits exactly this profile: a live, multi-megawatt solar+storage project in Southeast Europe. For us, the Europe story is not a slide — it is a system running on site.

Let's talk about it at Intersolar

We will argue this thesis in person at Intersolar Europe in Munich, 23-25 June — Booth C4.660F. If you own, build or finance solar+storage in Europe, book 20 minutes; let's talk about what orchestration creates on your asset.